En

En  De

De

Three charter models - three different answers to the same question: who bears the risk? This needs to be understood before capital enters the asset. Because afterwards - it is too late.

Imagine three investors. The first wants a stable cash flow, like a bond. The second is willing to take risk in pursuit of maximum returns at the top of the market. The third is looking for a long-term instrument with minimal operational involvement. All three are looking at the same thing - a vessel. But what they are buying are entirely different financial products.

That is the essence of the charter choice. Time charter, voyage charter, and bareboat are not merely operational contracts. They are instruments for distributing risk between the shipowner and the charterer. And the way that risk is allocated determines everything: cash flow, access to financing, asset value at sale, and, ultimately, the real return for the investor.

An investor who does not understand the difference between these three models will almost certainly encounter one of two outcomes: either overpaying for the illusion of stability, or leaving money on the table by missing a market window. Because the market does not wait.

The Charter as a Financial Instrument, Not Merely a Contract

Most people outside the shipping industry perceive a charter as a lease. That is not entirely accurate - and this inaccuracy can be costly. A lease implies a fixed object and a fixed payment. A charter is a system for distributing risks, revenues, and operational responsibilities that can be structured in very different ways.

For an investor, three things are of fundamental importance:

- Predictability of cash flow - how stable is the income from the asset, and how does it correlate with market volatility

- Operational burden - who manages the vessel, and who bears the costs of crew, maintenance, insurance, and regulatory compliance

- Impact on asset valuation - the existence of a long-term charter with a creditworthy charterer directly increases the value of the vessel in an S&P transaction

This is precisely why professional shipping fund managers - including those operating under Swiss and European institutional management standards - examine the charter book before looking at a vessel's technical specifications. An asset without a charter is simply steel. An asset with a properly structured charter is a financial instrument with a predictable profile.

On the other side of the table is always the charterer. But behind that word lie very different players:

- Trader - acquires tonnage for a specific trading position, typically on a short-term basis

- Operator - manages a fleet commercially, sub-charters vessels, and earns on the spread between rates

- Industrial user - a large cargo owner (an oil company, a mining holding) that requires guaranteed transportation of its own cargo

The credit quality of the charterer is perhaps the most underappreciated parameter when selecting a charter model. Even the most carefully structured deal will fall apart if the charterer exits the business two years down the line.

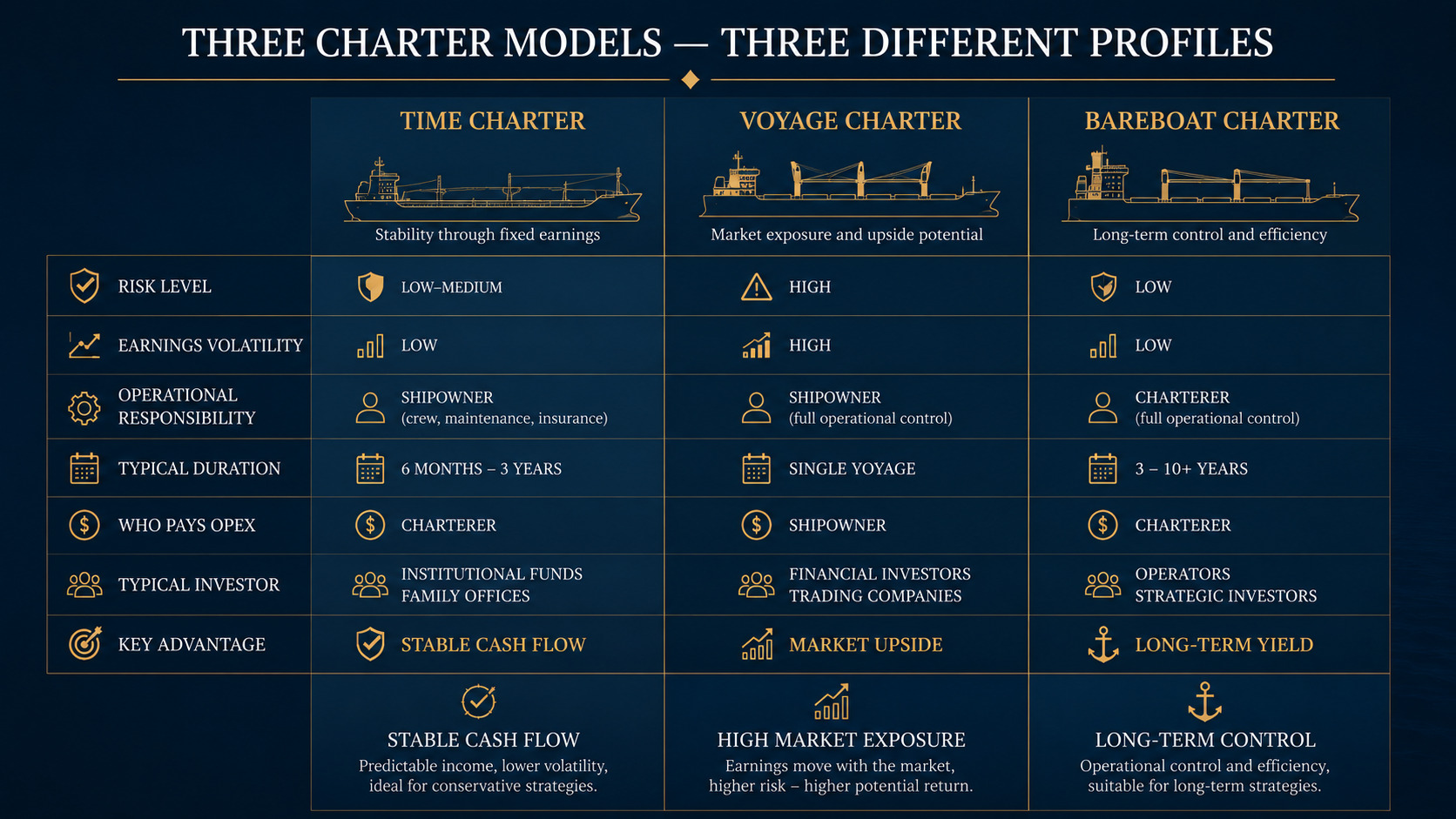

Time Charter: Stability with Caveats

How It Works

Under a time charter, the shipowner transfers the vessel to the charterer along with crew and management for a defined period - from several months to several years. The charterer pays a daily rate (hire) and assumes commercial management: choosing routes, cargoes, and ports. Bunker is the charterer's expense.

The shipowner, meanwhile, remains responsible for the technical condition of the vessel, the crew, and compliance with all maritime conventions. This is the shipowner's OPEX - operating costs that must be borne regardless of whether the vessel is working or undergoing repairs.

The Economics of a Time Charter

The key KPI for the investor here is TCE (Time Charter Equivalent). This is the time charter rate recalculated to account for all voyage costs, enabling comparability across different charter types.

Consider a simplified example. A vessel earns hire of $35,000 per day. At first glance - attractive. But the investor's actual income looks quite different:

- Daily hire rate: $35,000

- Less OPEX (crew, M&R, insurance, stores, administration): $8,500-10,000

- Less dry-dock reserve: $1,500-2,000

- Less offhire (technical idle time, averaging 2-3% of the year): ~$700-1,000

- Net operating income: ~$22,000-24,000 per day

And this is before debt service, if the vessel was acquired with financing. Because lenders want their share too.

Risks That Are Discussed Less Often

- Charterer credit risk - if the charterer stops paying hire, the shipowner is left with crew, running costs, and an idle vessel. This is the primary threat in the TC model

- Offhire - time when the vessel is not working due to technical problems is not paid by the charterer. Every day of offhire means lost hire plus continued OPEX

- Re-chartering risk - when the current TC expires, the shipowner must find a new charterer at prevailing market rates. If the market has fallen, income falls with it

Who Is Time Charter Suited For

Time charter is an instrument for the conservative investor. It works well:

- In structures with bank financing, which requires predictable cash flow to service debt

- For institutional funds with LP-investor reporting obligations

- When the counterparty is a creditworthy charterer with a rating, rather than a small trader

Time charter is not suitable for those who want to catch the peak of the market cycle. In a bull market, the hire rate is already locked in - all the upside goes to the charterer.

Voyage Charter: Freedom and Volatility

How It Works

Voyage charter operates on a fundamentally different logic. Here, what is being purchased is not time, but transportation: a specific cargo from point A to point B. The shipowner receives freight - payment for the voyage. But the shipowner also bears all variable costs: bunker, port dues, agency fees, canal tolls.

Key concepts without which voyage charter cannot be understood:

- Laytime - the agreed time allowed for loading and discharging, as specified in the charter

- Demurrage - a penalty paid by the cargo owner to the shipowner for each day in excess of laytime

- Despatch - a premium paid by the shipowner to the cargo owner if operations are completed ahead of laytime. Despatch is typically 50% of the demurrage rate

Demurrage is a separate P&L line item that is often underestimated. On certain routes it constitutes a substantial portion of voyage revenue. Delays in ports are not the exception - they are a fact of life in shipping.

The Economics of a Voyage Charter

Voyage P&L is straightforward: freight minus all voyage costs. But the devil is in the detail:

- Bunker costs - the largest variable. On a 15-day voyage consuming 40 tonnes per day, a $100/tonne difference in IFO price changes the voyage economics by $60,000

- Broker commission - standard 1.25% of freight per side, totalling 2.5%

- Address commission - often an additional 1.25-2.5% payable to the charterer

In a bull market, voyage charter outperforms time charter. When rates are rising, the shipowner in the spot market captures the maximum, while the TC player locked in a rate a month ago. But all of this works in precisely the opposite direction when the market falls.

Risks of Voyage Charter

- Bunker risk - the principal variable, which cannot be fully controlled. Hedging through bunker swaps helps, but adds complexity

- Port delays - congestion at major ports (China, Brazil, the Persian Gulf) can consume the entire voyage margin

- Operational burden - dispatching, coordination with stevedores, survey inspections, documentary formalities. Without a professional commercial team, this rapidly descends into chaos

Who Is Voyage Charter Suited For

Voyage charter is an instrument for those who understand the market from the inside:

- Operators with an in-house commercial team and broker network

- Speculative capital that knows how to work with volatility

- Players who combine spot exposure with hedging through FFAs (Forward Freight Agreements)

For a passive investor without operational infrastructure, entering voyage charter directly means taking on risks that cannot physically be managed.

Bareboat Charter: The Vessel as a Bare Asset

How It Works

A bareboat charter (BBC) is the transfer of a vessel without crew, without management - essentially without anything. The charterer receives a bare vessel and assumes full control: flag, ISM management, insurance, crew. The charterer becomes the temporary owner for the entire duration of the contract - typically 5 to 15 years.

The shipowner under a BBC receives a fixed hire and... is largely uninvolved in anything else. The primary concern is the condition of the vessel upon redelivery.

Bareboat as a Financial Instrument

The true nature of a BBC is not an operating lease but a financial lease. Especially when the structure in question is a BBCHP (Bareboat Charter with Hire Purchase) - an arrangement under which the charterer purchases the vessel at the end of the term at a pre-agreed price. In substance, this is an instalment sale with the seller retaining title on a temporary basis.

This is precisely why BBC is widely used in deal structuring:

- Chinese leasing - COSCO, CMB Leasing, ICBC purchase vessels and lease them back in BBC to the original shipowner. This releases capital while preserving operational control

- Sale & leaseback - the shipowner sells the fleet to a financial investor and receives it back under a BBC. A classic means of monetising the balance sheet

- KG funds and SPV structures - German and Scandinavian investment funds have historically been built on precisely the BBC logic

Risks of Bareboat Charter

- Technical condition on redelivery - the charterer has been operating the vessel for 10 years. What state is it in? This risk is managed through detailed survey protocols at redelivery, but cannot be eliminated entirely

- Credit risk over a long horizon - a 10-year contract means 10 years of dependence on the solvency of a single counterparty. If the charterer goes bankrupt in year 7, the shipowner gets back a vessel in unknown condition and with no hire stream

- Regulatory risk - CII, EU ETS, future decarbonisation requirements. Who bears the compliance costs? This must be clearly set out in the contract - otherwise it will become a point of dispute precisely when the costs turn out to be material

Who Is Bareboat Charter Suited For

- Financial investors with a long horizon who are interested in stable yield without operational involvement

- Leasing structures for which the vessel is collateral, not an operational asset

- Investors who want to enter the maritime sector through a structure close to infrastructure debt

Bareboat is not an instrument for those who want operational control over the asset or flexibility in decision-making.

Comparison of the Three Models

| Parameter | Time Charter | Voyage Charter | Bareboat |

|---|---|---|---|

| Who bears OPEX | Shipowner | Shipowner | Charterer |

| Bunker risk | Charterer | Shipowner | Charterer |

| Typical duration | 6 months - 3 years | Single voyage | 5-15 years |

| Income volatility | Low | High | Minimal |

| Operational burden | Medium | High | Minimal |

| Access to financing | Good | Difficult | Excellent |

| Impact on S&P valuation | Positive | Neutral | Very positive |

| Investor risk profile | Conservative | Speculative | Financial/leasing |

None of the models is universally superior. The right choice always depends on the specific investor, asset, market cycle, and investment horizon.

Matching a Model to Risk Appetite: A Practical Matrix

Theory is fine in seminars. In practice, the choice of charter model always comes down to a specific investor with specific goals and constraints. Let us consider four real-world scenarios.

Scenario A

An Institutional Investor Entering an Asset Through a Fund

The optimal model is a time charter with a creditworthy charterer, ideally with an index-linked rate adjustment. This provides predictable cash flow for LP reporting and creates a basis for bank financing. Credit analysis of the charterer matters more here than the technical condition of the vessel.

Scenario B

A Family Office Buying a Vessel Directly in a Bull Market

A mixed strategy: part of the fleet is fixed in TC for the medium term to protect base income, while the remainder operates on the spot (VC) to capture market upside. Hedging through FFAs reduces bunker risk on spot positions. Without a professional commercial team, this strategy is not viable.

Scenario B

A Family Office Buying a Vessel Directly in a Bull Market

A mixed strategy: part of the fleet is fixed in TC for the medium term to protect base income, while the remainder operates on the spot (VC) to capture market upside. Hedging through FFAs reduces bunker risk on spot positions. Without a professional commercial team, this strategy is not viable.

Scenario C

A Financial Investor Seeking Yield Without Operational Involvement

A BBC with a BBCHP structure over a long term (10-15 years) with a creditworthy operator. The economics resemble infrastructure debt: fixed yield, long horizon, minimal operational management. The key risk is the credit quality of the charterer and the legal structure of the redelivery conditions.

Scenario D

A Portfolio Approach - Diversification Within a Fleet

Professional operators rarely work within a single charter model. A realistic portfolio: 40-50% of tonnage in TC for stability, 30-40% on spot for volatile returns, 10-20% in BBC for a long-term anchor position. This is a dynamic strategy that changes with the market cycle - which is precisely why professional fund management here is not an option, but a necessity.

The charter book is not an administrative document. It is an investment strategy in legal form. This is why at Overhorn Swiss we analyse the charter structure of an asset before its technical condition.

What the Market Is Changing Right Now

The choice of charter model never exists in a vacuum. The 2024-2025 market has introduced several new variables that are changing the traditional logic.

CII and EU ETS: The Regulatory Factor Is Reshaping Cost Allocation

With the introduction of the Carbon Intensity Indicator (CII) and the inclusion of shipping in the European Emissions Trading System (EU ETS), a fundamental question has arisen: who pays for compliance? In a voyage charter - the answer is clear: it is the shipowner's cost. In a TC - it is a matter for negotiation, and it is increasingly being set out explicitly. In a BBC - formally the charterer, but if the CII rating deteriorates, the value of the asset falls for the shipowner.

Practical consequences:

- Vessels with a CII rating of D or E trade at a discount in S&P and find it harder to attract TC charterers

- EU ETS adds a direct monetary burden on voyages to and from European ports - this is already part of the voyage cost calculation

- New TC contracts now include "green clauses" allocating EUA (EU Allowances) costs between the parties

Sanctions Compliance Has Reshaped the TC Market

Since 2022, sanctions screening has become a mandatory part of TC due diligence. A creditworthy charterer now means not only financial soundness, but also jurisdiction, ownership structure, and OFAC/EU lists. A number of traditional TC players have dropped out of the market, creating a shortage of reliable charterers in certain segments.

Chinese Leasing Is Displacing the Classic BBC

Major Chinese leasing structures (ICBC Leasing, CMB Financial Leasing, COSCO Shipping) are aggressively expanding their portfolios through BBC structures. For the Western investor, this creates competition for quality BBC assets, but simultaneously - new opportunities for co-structuring deals.

TC Rates in Key Segments

Understanding the models is important. But equally important is understanding where the market stands right now:

- Bulker (Capesize, 12-month TC) - rates are historically volatile and sensitive to demand for coal and ore from Australia and Brazil

- Tanker (VLCC, Suezmax) - high spot returns in 2023-2024 created downward pressure on long-term TC rates: shipowners were reluctant to lock in at low levels

- Containership - normalisation after the 2021-2022 peak: long-term TC rates have stabilised, spot has weakened

Conclusion

The right charter model is not the one that generates the highest return on paper. It is the one that will not destroy your returns when the market turns against you. And at some point, it will. This is not pessimism - it is the mathematics of shipping cycles, which have existed for several centuries.

Time charter protects against volatility but limits upside. Voyage charter offers maximum market exposure but requires infrastructure and resilience. Bareboat turns a vessel into a financial instrument close to a bond - and carries the corresponding risks of a long horizon.

The choice between them is not a technical question. It is a question about who you are as an investor: what horizon, what level of volatility you are prepared to accept, and how much operational control you wish to retain. Once those three questions are answered, the right charter model becomes self-evident.

These are precisely the questions we begin with in every conversation with an investor at Overhorn Swiss.

We Will Match a Charter Strategy to Your Profile

The Overhorn Swiss AG team advises investors on the structuring of maritime assets in accordance with Swiss and European institutional management standards.

Contact the team