En

En  De

De

Most investors in shipping assets carefully calculate OPEX, model TCE, and negotiate senior debt rates. But few stop to think about what will happen on the day they exit the deal if the market is not where they expected it to be. This is precisely where RVI transforms from a dry insurance term into real money.

Overhorn Swiss AG · Lucerne, Switzerland · Ship Management & Shipping Finance

When the Market Drops Right Before Your Exit

Imagine: an investment fund enters a VLCC deal in 2019. The vessel is 8 years old, class confirmed, TCE at the time of purchase looks convincing. The horizon is 5 years, exit planned for 2024. The financial model is neatly assembled, IRR looks attractive. Everything is in order.

But by the time of sale, the secondhand market has softened. The vessel received a CII rating of "C" after the very first year under the new IMO methodology. Potential buyers demand a discount. Steel scrap prices have fallen. The result: minus $11-14 million against the expected NAV. This is not force majeure. This is residual risk that existed from day one of the deal and was simply overlooked.

What is an equity exit in ship finance? It is the moment when the holder of equity capital - whether a PE fund, a leasing company, or a private shipowner - sells the asset and locks in the final result. Everything that stands between the projected vessel value and its actual market price on that day is residual value risk. And that is exactly what RVI protects against.

The very nature of a shipping asset is such that its exit value depends on dozens of variables, many of which are outside the investor's control. Age, class, technical condition, regulatory status, freight market conditions, buyer financing availability - all of these shape the final price. RVI is the instrument that allows the minimum level of that price to be locked in before the deal is closed.

The equity exit is the moment of truth. And it is precisely at this moment that it becomes clear whether the deal was genuinely protected - or merely well modeled.

RVI - What Is It, Really? An Explanation Without an MBA

The phrase "residual value insurance" sounds as though it was invented specifically to put off everyone except actuaries. In practice, the mechanics are simple - and that is precisely why it is useful.

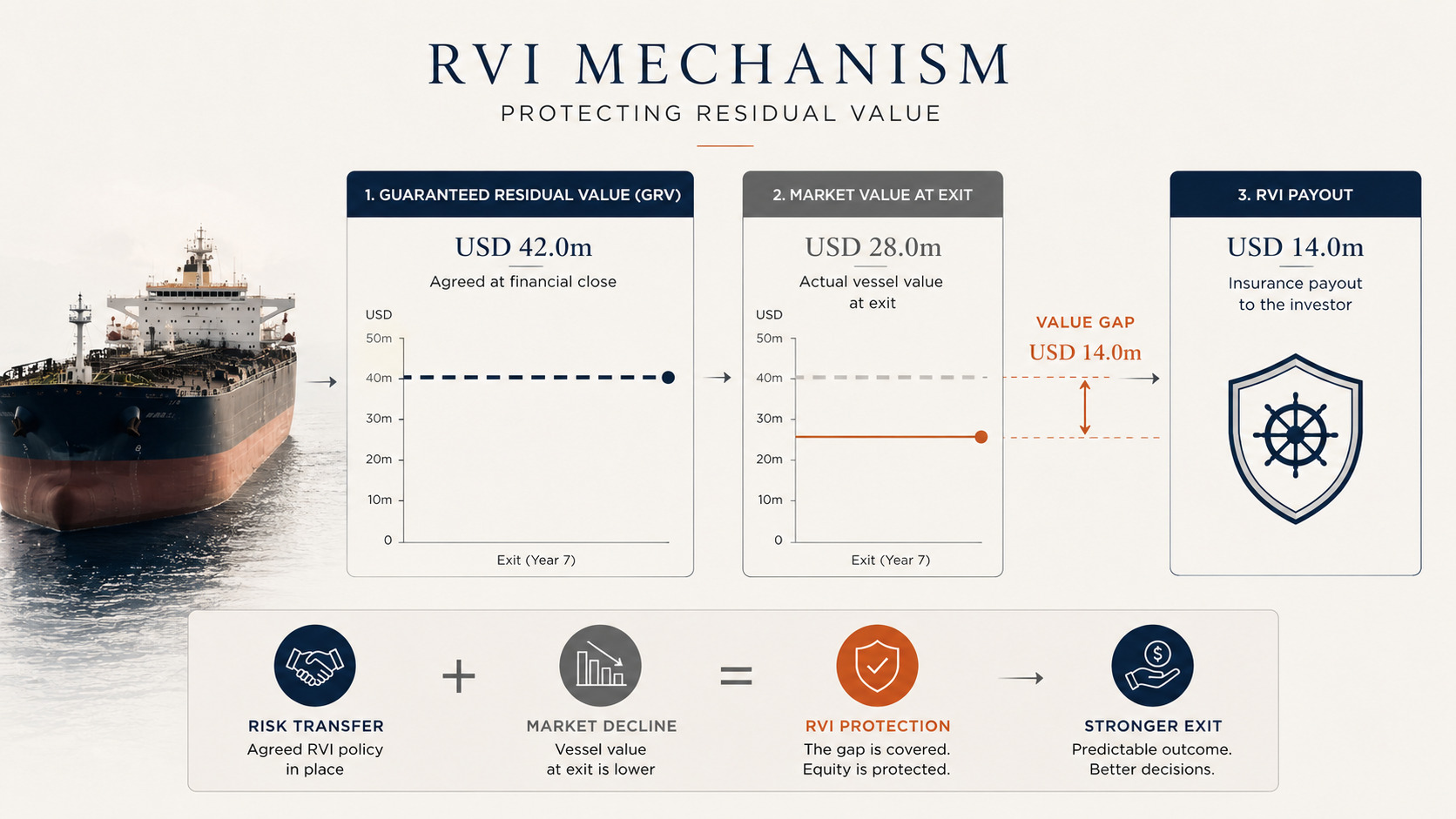

Residual Value Insurance (RVI) is an insurance policy under which the underwriter guarantees: if on a specified date the asset is worth less on the market than a pre-agreed sum (the Guaranteed Residual Value, or GRV), the difference will be paid out to the policyholder. It is not a loan, not a derivative contract, and not a guarantee. It is insurance - with a premium, a term, and payout conditions.

Key elements of an RVI policy

- GRV (Guaranteed Residual Value) - the minimum asset value guaranteed by the policy. Set at the time the contract is signed.

- Valuation date - the specific day on which the vessel's market value is determined and compared against the GRV.

- Payout - the difference between the GRV and the actual market value, if the market value is lower.

- Premium - paid in a lump sum or in installments, at the start of the term or in stages.

- Term - generally aligned with the investment horizon or the charter period.

Now the key question: how does RVI differ from what market participants already know?

| Instrument | What it protects | What it does not protect against |

|---|---|---|

| Hull & Machinery (H&M) | Physical damage to the vessel | Decline in market value |

| P&I Club | Third-party liability, environmental risk | Investment losses |

| Loss of Hire | Income during off-hire periods | Asset value at exit |

| RVI | Minimum asset value at the exit date | Operational risks, liability |

As you can see, RVI does not overlap with conventional marine insurance. It is an instrument from the world of finance, not from the world of technical operations. On the market, it is provided by specialist underwriters - predominantly through Lloyd's of London, as well as a number of European insurers working with alternative assets. Brokers specializing in such policies work in close collaboration with ship finance teams and valuers.

Without an understanding of the specifics of the shipping asset, the underwriter simply cannot properly assess the risk. And this is one of the reasons why RVI remains a niche instrument: the market demands expertise in two fields simultaneously.

Where RVI Fits in the Deal Structure

To understand the value of RVI, one must first understand how a typical shipping asset financing structure works. This is not an academic detour - without it, it is impossible to understand whose position the policy actually protects.

Capital Structure - Basic Framework

In most tanker and vessel transactions, capital is organized on a waterfall principle - a hierarchy of claims when distributing income and at exit:

- Senior Debt - bank financing, typically 55-70% of the vessel's value. First priority at exit. Repaid from sale proceeds first.

- Mezzanine Debt - subordinated loan or bonds, 5-15%. Receives payment after senior debt.

- Equity - 20-35%. Receives whatever remains after all debt is repaid. This is where residual value risk is concentrated.

In practice this means: if the vessel is sold for less than expected, equity suffers first. The senior lender is protected by LTV covenants and priority of claim. The equity holder is not.

Example: equity loss calculation when asset value falls

A vessel is purchased for $60 million. Senior debt: $38 million. Equity: $22 million. After 6 years, market value: $34 million. After debt repayment ($32 million remaining balance after amortization), the equity holder receives $2 million instead of the expected $13-15 million. Without RVI, this is simply a loss. With RVI at a GRV of $45 million, a payout of $11 million covers most of the gap.

When RVI Is Integrated into the Deal

RVI fits most naturally into the following structures:

- Bareboat charter (BB) - the charterer bears operating costs; the owner bears the residual value risk. RVI protects precisely this owner risk.

- Sale-leaseback - a shipowner sells a vessel to a financial company and charters it back. The financial company acquires the asset, taking on the risk of its value at the end of the lease. RVI is a natural hedge for this risk.

- JOLCO (Japanese Operating Lease with Call Option) - Japanese investors bear residual value risk structurally. RVI reduces their actual exposure.

- PE funds with a fixed horizon - obliged to exit within a set timeframe regardless of market conditions. For them, RVI is not an option but part of investment discipline.

In structures where there is a hard exit date and no ability to "wait out" a weak market, RVI ceases to be an additional cost line and becomes a condition for the deal itself.

What Determines the Residual Value of a Tanker

Before insuring a risk, one must understand what it consists of. The residual value of a vessel is not a random figure. It is determined by a combination of factors, each of which can be measured, assessed - and in some cases - partially controlled.

Technical and Operational Factors

- Vessel age - the most predictable factor. The depreciation curve for tankers is reasonably well established, though crises distort it.

- Class and condition - confirmed class (DNV, Lloyd's, BV) with no open recommendations significantly affects asset liquidity.

- Drydock history - scheduled dry-docking completed on time reduces the discount at sale.

- Technical equipment - the presence of BWTS, scrubbers, and energy efficiency monitoring systems affects both operating costs and buyer attractiveness.

- PSC history - port state control deficiencies are stored in databases and visible to any prospective buyer.

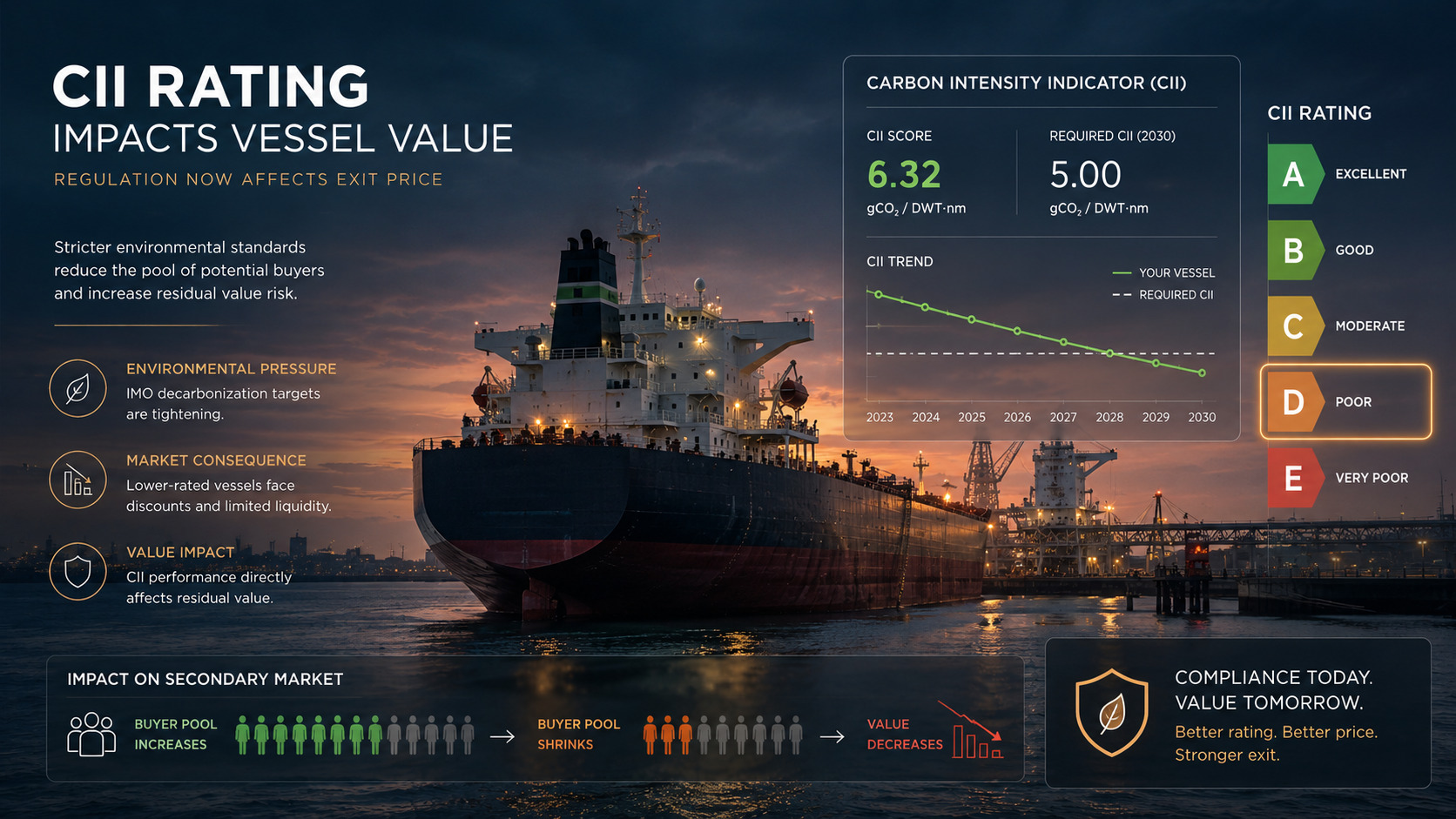

The Regulatory Factor - A New and Underestimated Variable

Before 2023, regulatory risk was abstract. Now it is very concrete. The CII (Carbon Intensity Indicator) rating is assigned annually and directly affects the commercial attractiveness of a vessel:

| CII Rating | Meaning | Impact on value |

|---|---|---|

| A / B | Better than IMO requirements | Premium to market, high liquidity |

| C | Meets requirements | Neutral |

| D | Below requirements, warning | 5-12% discount, narrowed buyer pool |

| E | Significantly below requirements | Material discount, restricted market |

The RVI underwriter takes the CII trajectory into account when calculating the GRV. A vessel with a consistent B rating will receive more favorable policy terms than a comparable vessel with a history of D ratings. This is a direct link between operational discipline and the cost of insurance protection.

VLCC vs. MR - Two Different Risk Curves

| Parameter | VLCC (Very Large Crude Carrier) | MR Tanker (Medium Range) |

|---|---|---|

| Average newbuilding price | $120-140 million | $45-55 million |

| Secondhand market depth | Limited, large individual transactions | Liquid, broad buyer pool |

| Value volatility | High, correlated with crude oil routes | Moderate, diversified across routes |

| Scrap value | High in absolute terms | Moderate, serves as a price floor |

| RVI complexity | Higher, requires specialist underwriting | More standardized |

Practical conclusion: for VLCCs, RVI is critically important precisely because of high volatility and a narrow buyer pool. For MR tankers the instrument is also relevant, but underwriters are prepared to work on more standardized terms.

Who Needs RVI - and Who Does Not

An honest discussion of the instrument includes acknowledging its limitations. Not every deal needs RVI - and this is important to understand before beginning negotiations with an underwriter.

Who Needs RVI

- PE funds with a fixed horizon (5-8 years) - obliged to exit within a specific timeframe. Cannot afford to wait for a market recovery. RVI provides predictability for the minimum exit value.

- Leasing companies - especially those operating under sale-leaseback or JOLCO structures. They bear residual value risk structurally - RVI reduces actual exposure without changing the legal framework of the deal.

- Shipowners on long-term TC-out - they have chartered out their vessel for 7-10 years and know it will be returned in a specific year. The value at that point is unknown. RVI fixes the minimum.

- Lenders requiring equity protection - in certain structures, a bank requires the equity investor to have RVI as a condition for reducing the margin or increasing LTV. The instrument becomes part of the credit package.

- Investors entering at market peak - buying a vessel in a period of high freight rates and high secondhand prices creates an elevated risk of "buying high, selling low." RVI is insurance against exactly this scenario.

Who Most Likely Does Not Need RVI

- An opportunistic spot operator with a 1-3 year horizon and a willingness to sell the vessel at any time the market allows. There is no hard exit date - and therefore no hard risk.

- A shipowner with a diversified fleet, managing 20+ vessels and treating residual risk as a portfolio matter - naturally averaging out over time.

- Deals with a very short horizon (under 2 years) - the market uncertainty value over this period is too small to justify the premium.

- Assets with a high scrap value relative to market price - if the vessel is 20+ years old and its scrap value covers 80-90% of market value, the downside is effectively limited.

A simple test: does your deal need RVI?

Answer three questions:

- Is there a hard exit date in the deal structure that cannot be moved?

- Is the investment horizon 4 years or longer?

- Is the gap between the expected and the minimum acceptable exit value material to the return?

If two out of three answers are "yes" - a conversation with an underwriter is worth having.

What RVI Costs and How to Negotiate with an Underwriter

RVI is not exchange-traded. There is no standard price list, no public indices. Every policy is the result of a negotiation grounded in the assessment of a specific asset, a specific structure, and a specific market. This is precisely why preparation for these negotiations matters as much as the negotiations themselves.

Factors Affecting the Premium

- Vessel type - VLCC, Suezmax, Aframax, MR, Product Tanker. More liquid markets produce more competitive terms.

- Vessel age at the exit date - the older the vessel at the end of the policy term, the higher the risk for the underwriter.

- GRV as a ratio to current market value - coverage at 60% of current value will cost considerably less than coverage at 85%.

- Policy term - a longer horizon means more uncertainty, which means a higher premium.

- Operational history - CII ratings, PSC record, operator.

- Regulatory landscape - vessels subject to EU ETS or requiring additional investment to comply with IMO 2030 attract a higher premium.

Market Benchmarks

Without reference to a specific deal, only very broad benchmarks can be given. The RVI premium for a typical tanker asset with a 5-7 year horizon and coverage of 60-75% of current value has historically ranged from 1.5-4% of GRV per year - depending on all of the factors listed. This is not negligible. But it is also not comparable to the potential losses from a poorly timed exit.

What You Need to Prepare for the Underwriter

This is not a general conversation. The underwriter will work with real data. The minimum documentation package includes:

- Current technical report (Class Status, Survey Records)

- CII and EEXI calculation history for the past 2-3 years

- Vessel charter history (operators, routes, cargo types)

- PSC history (last 36 months)

- Deal financial model with capital structure description

- Independent vessel valuation (from an accredited appraiser)

The underwriter is accepting precisely the risk you cannot bear yourself. And they want to understand that risk in as much detail as you do. A well-prepared package is not bureaucracy. It is the language of trust.

Who Operates in This Market

The RVI market for shipping assets is narrow. The main players are specialist Lloyd's of London syndicates, a number of European insurers (particularly Scandinavian and German players with maritime expertise), and several global brokers specializing in alternative asset insurance. Approaching this market through a conventional insurance broker without ship finance expertise is a near-guaranteed waste of time.

Three Scenarios Where RVI Saved the Deal

Abstract arguments in favor of an insurance instrument are thankless. Far more persuasive are concrete situations. We do not name parties or disclose details of specific transactions, but the scenarios described below reflect real patterns that investors in shipping assets encounter.

Scenario 1

Forced Exit into a Weak Secondhand Market

A European PE fund with a mandate for alternative infrastructure assets acquired an Aframax in 2018. Fund horizon: 7 years, mandatory exit by 2025 under LPA terms. By 2024 the secondhand market in the Aframax segment had cooled: excess tonnage, declining route volumes, and growing uncertainty around sulfur and CO2 requirements for vessels over 12 years old.

An RVI policy structured at the time of purchase with a GRV set at 62% of the acquisition price was triggered: the market price at the time of sale was 18% below the GRV. The policy payout recovered most of the gap and allowed the fund to close the deal within its target return range.

Scenario 2

CII Rating of "D" - and a 30% Loss of Buyers

A Japanese leasing company structured a Product Tanker deal under a JOLCO arrangement. Upon expiry of the lease, the vessel was to be sold on the open market. Two years before the end of the term, the vessel received a CII rating of "D" - as a result of a change in the charterer's operational profile (a shift to shorter routes with more frequent port calls, which worsened carbon intensity metrics).

The pool of potential buyers shrank: a number of European operators had introduced internal standards excluding vessels rated below "C." The final sale price came in below expectations. RVI compensated the gap between the projected and actual value, preserving the deal economics for the Japanese investors.

Scenario 3

Early Charter Termination by the Counterparty

A shipowner placed a VLCC on a long-term bareboat charter to a major trader for 8 years. In year 5, the trader initiated early termination of the agreement due to fleet restructuring - paying the contractually stipulated penalty, but with no obligation regarding the vessel's redelivery value. The shipowner was forced to sell at an unfavorable time.

The RVI policy, written for 8 years with the valuation date at the end of the term, contained a clause treating early charter termination as a valuation trigger. The payout was made based on the market valuation at the date of actual sale. The shipowner received compensation for the gap between the GRV and the market price, avoiding balance sheet losses.

All three scenarios share one thing: the risk was known in advance, structured into the policy, and turned from a catastrophic loss into a manageable insurance claim. That is precisely the purpose of the instrument - not to eliminate risk, but to make it predictable and bounded.

The Instrument Your Deal Is Missing

RVI is not the answer to every question in ship finance. But for a certain class of deals - those with a fixed horizon, complex capital structure, and material residual value risk - it is the element whose absence leaves equity protection incomplete.

Most market participants carefully work through the OPEX budget, freight strategy, debt structure, and regulatory compliance. Residual value, meanwhile, is modeled as one of several Excel scenarios - and that is where the work ends. RVI is the next step: turning scenario analysis into real financial protection.

Investor Checklist: 5 Questions Before Closing a Deal

- Is there a hard exit date in the deal structure that cannot be moved at your own discretion?

- Is the gap between the expected and the minimum acceptable exit price more than 15% of invested equity?

- Is the vessel exposed to regulatory risk (CII, EEXI, EU ETS) that could materially narrow the buyer pool at the exit date?

- Is the secondhand market for this vessel type volatile or limited in depth?

- Do lenders or LP investors require additional protection for the equity position?

If at least three answers are "yes," the conversation about RVI should begin before the final term sheet - not after it is signed. Precisely because policy terms are negotiated when all deal data is available - and the earlier the dialogue with the underwriter begins, the more room there is to maneuver.

Remember: RVI is not an expense. It is part of the return structure. The cost of the policy is built into the model in the same way as the cost of Hull insurance or P&I Club membership - and it affects the final IRR no more than sound OPEX management does. But unlike saving on lubricating oils, protecting residual value can preserve the entire deal.

A good deal is not one that started well. It is one that ended well.

Let's Talk About Your Deal

The Overhorn Swiss AG team structures maritime investments with a focus on the full investment cycle - from asset selection and financing to exit strategy and equity protection. We work with RVI as part of the investment structure, not as a standalone insurance product.

If your deal contains residual value risk that currently lives only in Excel, we are ready to discuss how to structure it properly.