En

En  De

De

When did you last carefully read your Hull & Machinery policy? Not sign it, not renew it - but actually read it, pencil in hand, running through scenarios and asking yourself honestly: "What happens if the vessel runs aground tomorrow?"

A vessel's insurance package is not a checkbox on an operational checklist. It is the financial immunity of an asset worth anywhere from $20 to $120 million. The issue is not whether the vessel is insured. The issue is whether the package can withstand a real blow.

A few years ago, a shipowner in the North Sea discovered that his H&M covered the repair but not the lost freight for 47 days of downtime. The Loss of Hire policy had a 30-day waiting period and an understated daily rate. The result was a cash shortfall of $800,000 despite a formally "complete" insurance package.

Below is a detailed breakdown of each element of the package, along with specific questions to help you identify weak spots before a claims event does it for you.

The Vessel Insurance Package - Why "Package" and Not "Policy"

From the outset, many shipowners are misled by the very word "insurance." A single policy - like a single layer of clothing in a storm - is simply not enough.

A full insurance package for a tanker or bulker consists of four interrelated elements:

- Hull & Machinery (H&M) - insurance of the hull, engine room, and equipment against physical damage. This is the vessel's "body."

- Protection & Indemnity (P&I) - liability insurance covering third parties: crew, cargo, the environment, collisions. This is the vessel's "actions" in the world.

- Loss of Hire (LoH) - compensation for lost freight during periods of forced downtime. This is the "circulatory system" of cash flow.

- War Risk - coverage for risks excluded from standard policies: mines, capture, military action, piracy. This is the "armor" for dangerous routes.

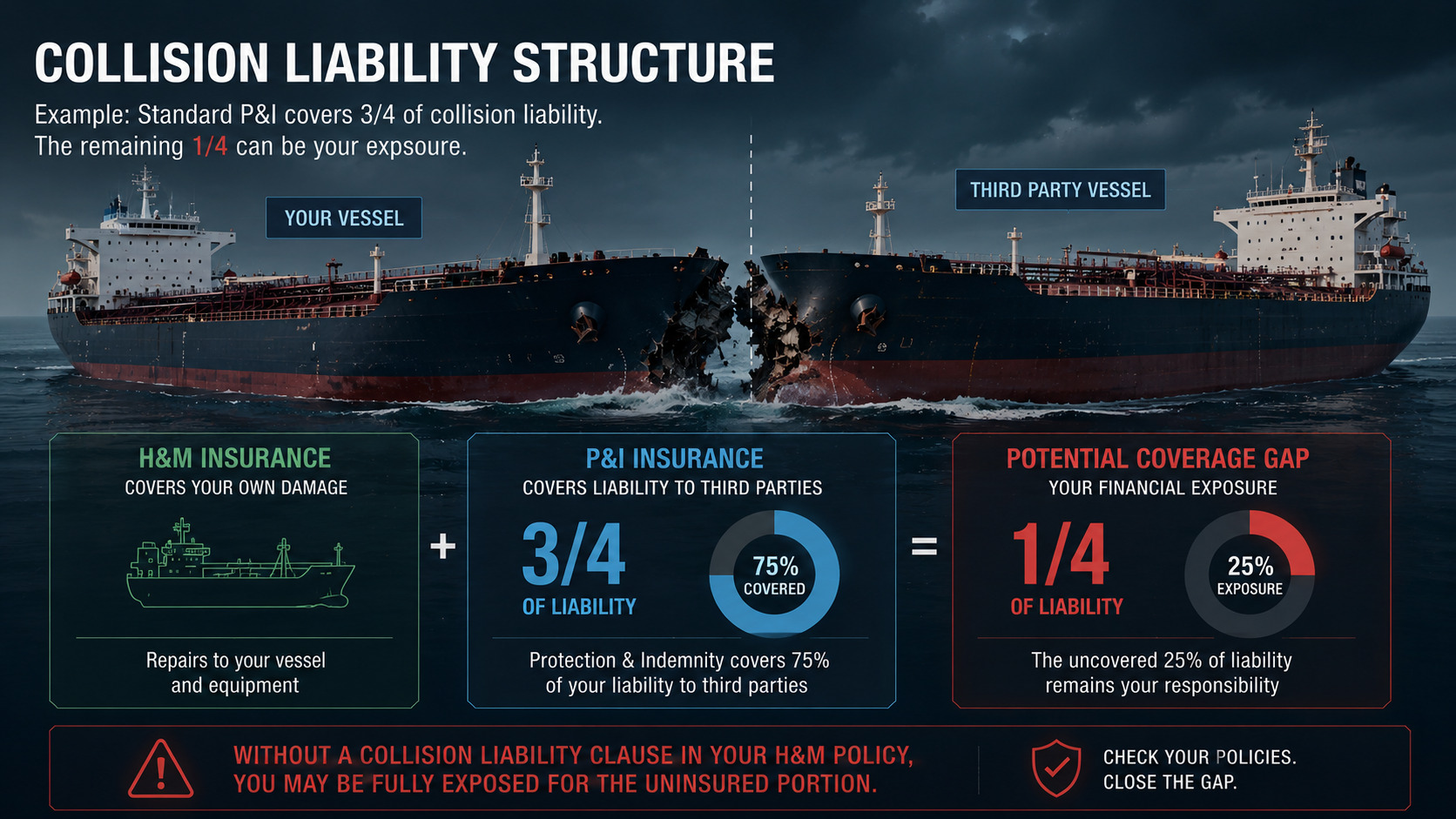

It is critically important to understand that these four elements do not duplicate one another - they complement each other. But there are gaps between them through which real losses slip. A classic example is the boundary between H&M and P&I in the event of a collision. H&M covers damage to your vessel; P&I covers liability to the third party. But the standard P&I covers only 3/4 of collision liability. The remaining quarter is yours to bear - unless your H&M policy contains a specific clause addressing it.

As you can see, the package is a system, not a collection of documents. And it must be tested as a system.

H&M Under Stress: A Test of Hull Insurance Robustness

Do not be too quick to celebrate the agreed insured value. What is written in the policy and what the underwriter will actually pay out are often two different numbers.

Where Underinsurance Hides

The insured value in H&M is agreed at the time the contract is signed. But markets change. Aframax tankers that were worth $28-32 million in 2020 reached $60-65 million on the secondhand market by 2024. If your agreed value has not been updated in the past two to three years, you are already underinsured.

Three key concepts worth distinguishing:

- Agreed value - the sum for which the vessel is insured under the contract

- Market value - the actual price of the vessel on the secondhand (S&P) market

- Replacement value - the cost of building an equivalent new vessel

If the agreed value is below market value, in the event of a constructive total loss you will receive less than you have lost.

Scenario 1 - Constructive Total Loss (CTL)

A constructive total loss occurs when the cost of repair exceeds the agreed insured value - typically the threshold is 70-80%, depending on the policy terms. This seems straightforward. But the devil is in the details:

- Who pays for the survey to assess the damage and determine CTL?

- Who bears the cost of temporary repairs pending a CTL decision?

- Who pays for scrapping and towage to the demolition site?

- Is wreck removal included in the coverage, or is it a separate line item?

Scenario 2 - Particular Average

Partial loss is the most common claims event in shipping. Here it is important to know:

- The size of the deductible - is it a fixed amount or a percentage of the insured value?

- Whether there are age-related exclusions - for vessels over 15 years old, some underwriters apply increased deductions

- Whether dry-dock costs are covered if the vessel was sent there as a result of an insured event

- How recurring engine room defects are handled - is there a second occurrence exclusion?

Scenario 3 - Port Delay Following a Grounding

A vessel touches the bottom while berthing in port. The damage is minor - a scratch on a ballast tank. But the port requires an underwater survey before departure. The survey takes 3 days. Who bears the cost?

The answer depends on the specific policy terms. It often turns out that the survey costs are yours to bear if the damage has not been formally confirmed.

The Role of Class

One important point that is often overlooked: suspension of the class certificate automatically triggers suspension of H&M coverage. A vessel without class is an uninsured vessel. An overdue intermediate survey or an overdue dry dock can lead to exactly this situation.

Key question: Has your broker requested an updated market valuation in the past 12 months?

P&I: The Club Is There - But Will It Cover Your Case?

A P&I Club is not an insurance company in the conventional sense. It is a mutual club in which the rules are set by the members themselves. That is why the details matter enormously.

The P&I Structure: How It Actually Works

Unlike commercial insurance, a P&I Club operates on a mutual basis:

- Advance call - the base contribution paid at the beginning of the year, calculated on the basis of the club's projected losses

- Supplementary call - an additional contribution if losses exceed the projection; it can reach up to 50% of the advance call

- Club discretion - some cases are covered not as a matter of right but "ex gratia," at the discretion of the club's directors

This means that formally full coverage does not guarantee automatic payment in every case.

Scenario 1 - Collision and the Infamous Quarter

In a collision between two vessels, the standard H&M policy covers 3/4 of your liability to the other vessel through what is known as the Running Down Clause (RDC). The remaining 1/4 is covered by P&I - but only if your H&M policy contains the appropriate 4/4 collision liability clause.

If no such clause exists, 25% of the liability remains uncovered. In a collision involving Suezmax-class vessels, that "quarter" can amount to millions of dollars.

Scenario 2 - Oil Spill

An oil spill is not simply a claims event. It is a chain of liabilities:

- CLC (Civil Liability Convention) - the shipowner's direct liability

- IOPC Fund - an international fund covering losses beyond the CLC limits

- P&I Club - payments within the club's limits (for IG Group clubs - up to $1 billion)

What remains with the shipowner: costs incurred between the event and confirmation of coverage; regulatory fines that P&I does not cover in certain jurisdictions; reputational and legal costs.

Scenario 3 - Vessel Arrest and the Crew

A vessel is arrested on a cargo claim in the port of Houston. The crew has been on board for three weeks. Who pays for crew maintenance, repatriation, and relief?

P&I covers these costs - but only if the shipowner notified the club promptly and followed its instructions. Independent action taken without the club's approval may result in a denial of coverage.

Scenario 4 - Cargo Claim in Excess of Expectations

The cargo is declared as "general chemicals," but in practice it is a specialized chemical product with a market value three times higher than the standard rate. When the cargo is damaged, the claim exceeds what was factored in when calculating contributions.

The question is: has the cargo type been correctly declared in the P&I? Does the vessel's actual trading pattern comply with the club membership terms?

Key question: Is your P&I Club a member of the International Group of P&I Clubs - and do you understand the difference between an IG club and an independent club in terms of limits and reinsurance?

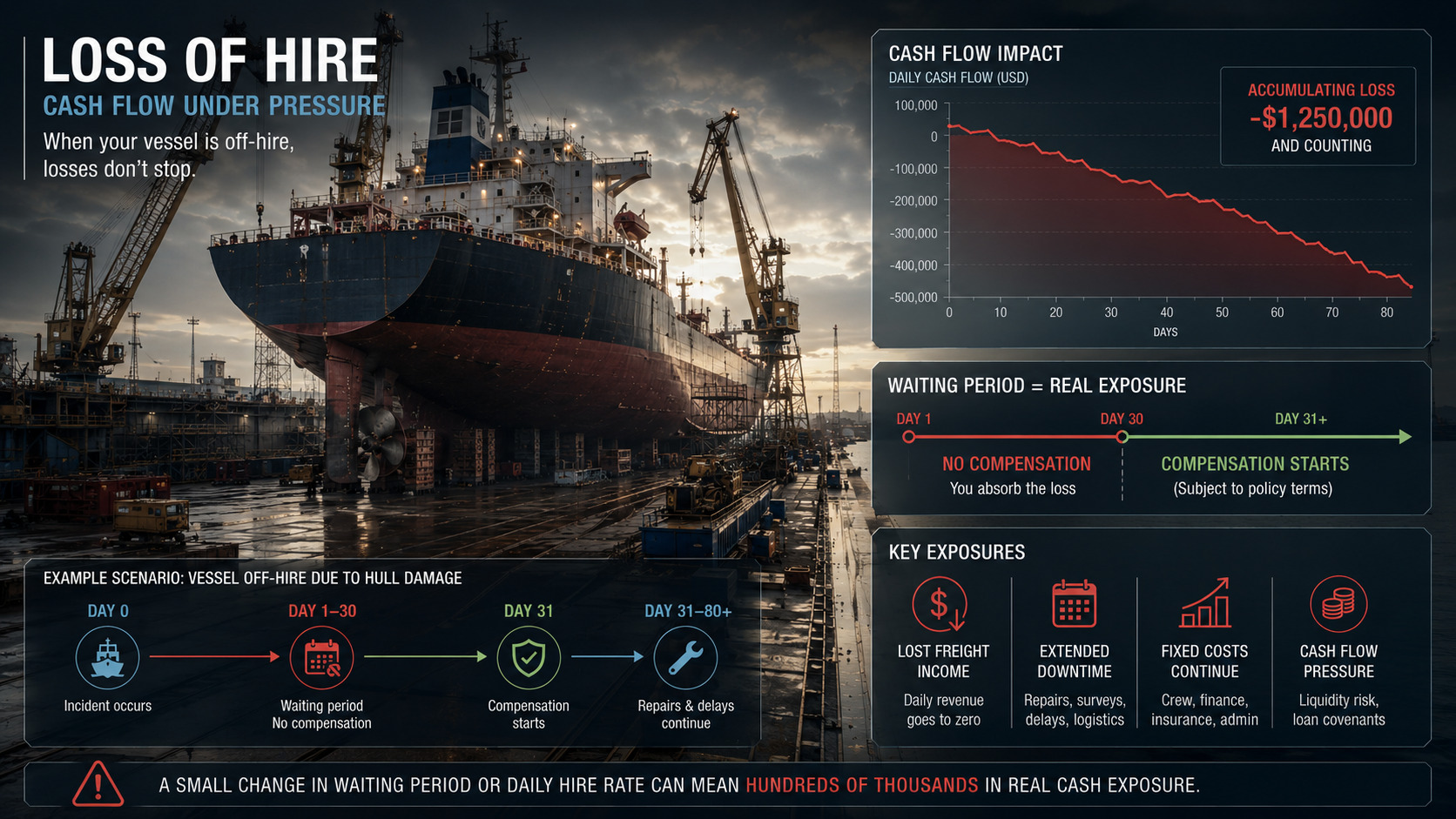

Loss of Hire: The Invisible Loss That Destroys Cash Flow

Loss of freight is the type of loss that is not immediately visible. The vessel sits idle. Costs keep running. Freight revenue stops. And this is precisely where good insurance differs from a piece of attractive paperwork.

The Mechanics of Loss of Hire: Three Key Parameters

| Parameter | What It Means | Typical Values | Risk If Set Incorrectly |

|---|---|---|---|

| Waiting period (franchise) | Number of idle days before payments commence | 14, 21, or 30 days | If the repair takes 25 days and the franchise is 30 days, no payment is made |

| Daily rate | The amount of daily compensation | TC rate or OPEX | An understated rate at inception means undercoverage at the time of loss |

| Maximum period | The maximum number of days of indemnity | 90, 180, or 365 days | A lengthy repair in China may exceed the limit |

Scenario 1 - Extended Repair Following a Casualty

An MR-class tanker sustains rudder damage while entering port. H&M recognizes it as a covered event. The process begins: survey, negotiation with the underwriter, sourcing a shipyard, queuing for dry dock.

A realistic timeline for a typical case:

- Days 1-7: survey and documentation of damage

- Days 8-14: negotiations with the underwriter on the scope of repairs

- Days 15-21: finding an available shipyard and agreeing on a schedule

- Days 22-28: towage or transit to the shipyard

- Days 29-60: the actual repair

Total: 45 to 70 days. If your waiting period is 30 days, Loss of Hire begins to pay from day 31. The first month of downtime is yours.

Scenario 2 - Repair in an Inconvenient Port

The same casualty, but the vessel is in Bangkok and the nearest suitable shipyard is in Singapore. The difference in repair time between a yard in South Korea and one in Europe can be 3-4 weeks. These are additional weeks for which Loss of Hire either pays - or has already reached its limit.

A Common Mistake at Inception

Shipowners often understate the daily rate when taking out LoH coverage in order to save on premiums. The logic is understandable. But the outcome is devastating: in the event of an actual loss, the compensation covers only part of the real losses.

The correct approach to setting the daily rate:

- For vessels on time charter: use the current TC hire rate

- For vessels trading on the spot market: base it on average earnings over the past 12 months

- The minimum justified baseline: the vessel's OPEX (operating expenses per day) - this at least prevents a negative cash position

Key question: Is your waiting period 14 or 30 days - and how does that compare with the average dry-dock turnaround time for your vessel type in your trading region?

War Risk: The Risk Map Has Changed

Only a few years ago, War Risk was little more than a formality for most shipowners. Today, routes through the Red Sea, the Strait of Hormuz, and the eastern Mediterranean are no longer "exotic." The market has already priced this in: War Risk premiums on certain routes have risen 10 to 20 times since 2023.

What Standard War Risk Covers

The standard Institute War Clauses (Hulls) include:

- Damage or loss arising from acts of war, mines, torpedoes

- Capture, seizure, or detention by hostile forces

- Piracy (under certain policy versions)

- Civil unrest and terrorist acts (subject to a specific clause)

What Basic War Risk Does NOT Cover - and This Is Critical

- Confiscation or nationalization by the flag state or the state of the port of destination

- Damage from nuclear weapons

- Losses resulting from a sanctions regime (depending on the clauses)

- Cyber attacks, if classified as acts of war

Current Map of Additional High-Risk Zones (2024-2025)

| Region | Nature of Risk | JWC Status | Indicative Additional Premium |

|---|---|---|---|

| Red Sea / Bab-el-Mandeb Strait | Drone strikes, Houthi missiles | Listed Area | 0.5-1.5% of insured value per voyage |

| Persian Gulf / Strait of Hormuz | Iranian activity, vessel seizures | Listed Area | 0.1-0.5% per voyage |

| Black Sea (Ukrainian waters) | Mines, military action | Listed Area | 1.0-3.0% per voyage |

| Eastern Mediterranean | Regional instability | Under monitoring | On request from underwriter |

Scenario 1 - Forced Deviation from Route

A vessel is transiting the Bab-el-Mandeb Strait. The master decides to alter course and bypass the Red Sea via the Cape of Good Hope. The additional distance means 12-14 extra days at sea, additional bunker costs, and a time-charter event forfeited.

The question is: who compensates for these costs? War Risk covers losses from a realized threat. A precautionary deviation is a separate matter - one that requires a specific clause in the policy or agreement with the charterer under the BIMCO war clause.

Scenario 2 - Detention by a State

A vessel is detained by authorities in a port of a country under sanctions pressure. Does this constitute "detention by hostile forces" under War Risk - or is it "arrest by a state" for political reasons, which is excluded from coverage?

The line between these two qualifications in the policy is a fine one. And it is the underwriter, not the shipowner, who draws it.

JWC Listed Areas: Keeping Up to Date Is Your Responsibility

The Joint War Committee regularly updates its list of high-risk areas. When a vessel enters a Listed Area:

- The insurer must be notified at least 48 hours in advance (in some policies - 7 days)

- An additional premium is calculated and paid

- Only then does coverage extend to that area

If notification was not given in time, the vessel enters the area without War Risk coverage. Formally. And in practice.

Key question: Does your War Risk update automatically when JWC Listed Areas change - or does it require a manual endorsement? And who in your organization is responsible for this?

A Practical Stress Test: Five Axes of Review

We propose a concrete tool, not a theory. Check your package across five axes - and you will see where the real vulnerabilities lie.

Axis 1 - Adequacy of Insured Value

- When was the agreed value in H&M last updated?

- Has the broker requested an independent market valuation?

- Has the insured value been benchmarked against actual transactions in the S&P market?

Best practice: review the value annually or whenever there is a significant market shift.

Axis 2 - Completeness of Coverage: Identifying Gaps

- Is there a 4/4 collision liability clause in H&M - or only the standard 3/4?

- Does P&I cover all cargo types actually carried by the vessel?

- Are the exclusions in H&M and P&I aligned - are there areas covered by neither?

Axis 3 - Liquidity at the Time of Loss

- How long will it realistically take to receive the first payment from the underwriter - 30 days, 90 days?

- Does the company have bridge financing or a reserve to cover the waiting period?

- Does the P&I policy allow for interim payments before the investigation is concluded?

Axis 4 - War Risk Currency

- Do the vessel's trading routes correspond to the current JWC Listed Areas?

- Is the notification procedure upon entering a risk zone specified in the policy?

- Does War Risk include piracy, drone attacks, and cyber incidents of a military nature?

Axis 5 - Loss of Hire Calibration

- Does the daily rate in LoH reflect the vessel's actual earnings (or at least OPEX)?

- Is the waiting period appropriate given the average repair time for your vessel type?

- Is the maximum indemnity period sufficient - accounting for possible shipyard delays?

Summary Assessment Matrix

| Review Axis | Green Zone | Amber Zone | Red Zone |

|---|---|---|---|

| H&M Insured Value | Updated less than 12 months ago | 12-24 months without review | More than 2 years, or market has risen 20%+ |

| Completeness of Coverage | Gap analysis completed, 4/4 CLC in place | Analysis conducted but some time ago | Gap analysis never performed |

| Liquidity | Reserve for 90+ days or bridge facility | Reserve for 30-60 days | No reserve, relying solely on insurance |

| War Risk | Policy current, notification procedure in place | Policy in place, procedure not formalized | Basic policy, routes not reviewed |

| Loss of Hire | Rate current, franchise 14 days or less | Rate understated or franchise 21-30 days | Rate not updated, franchise 30+ days |

Insurance Audit as Part of Operational Discipline

A stress test of the insurance package is not a one-time event. It is an annual practice that should be built into the operational cycle of fleet management.

The right time to conduct an audit is 60-90 days before the policy renewal date. This provides enough time not simply to roll over the existing coverage, but to perform a gap analysis, obtain alternative quotations, and agree on changes with the club and underwriters.

Ideally, an insurance audit should be treated in the same way as a technical audit before dry dock. Both instruments protect the same asset - just from different angles.

At Overhorn Swiss AG, insurance monitoring is part of our comprehensive approach to vessel management: we track the currency of coverage, compliance of trading routes with War Risk conditions, and the alignment of LoH with the actual financial profile of each vessel.

If you would like to identify exactly where your insurance package is vulnerable, we are ready to conduct an independent review. Contact us: info@overhorn.ch / +41 79 828 07 07.

A good insurance package is invisible in calm times. Its value becomes apparent on one specific day - when something goes wrong. And that is precisely why it needs to be reviewed now. You can be sure of that.